HELOC Runoff is Leading to Broader Consumer Portfolio Runoff

As part of the BRD Insights blog series, today we look into the asset mix at banks of different sizes. Asset mix is a telling indication of the strategic focus of banks and is the primary driver of banking economics. Portfolios focused entirely on mortgage can expect different losses, returns, capital constraints and operational complexities than a bank that focuses primarily on commercial and industrial development.

The wealth of knowledge in the asset mix data can’t be boiled down to a single blog post. To simplify matters, today’s post will be focused on explaining the decreasing consumer concentration at the “Big 4” Banks (> $500 B in total assets).

Figure 1 — Commercial includes multifamily, commercial and industrial, commercial real estate, farm loans, farmland loans, lease financing receivables, and construction and development. Consumer includes mortgage (first and junior), Auto, Card, HELOC, and individual other.

Banks with more than $500 B in assets had over 70% of assets concentrated in consumer in 2010 – more than any other banking segment for any period since 2003. A decade later, the asset mix at these banks has shifted more toward commercial loans, though 56.5% of loans are consumer assets as of the end of 2019. This shift is a result of growth in commercial portfolios combined with decreases in consumer portfolios (CAGR of 4.2% and -2.2%, respectively). These shrinking consumer portfolios lead to a smaller market share for the biggest banks in consumer overall.

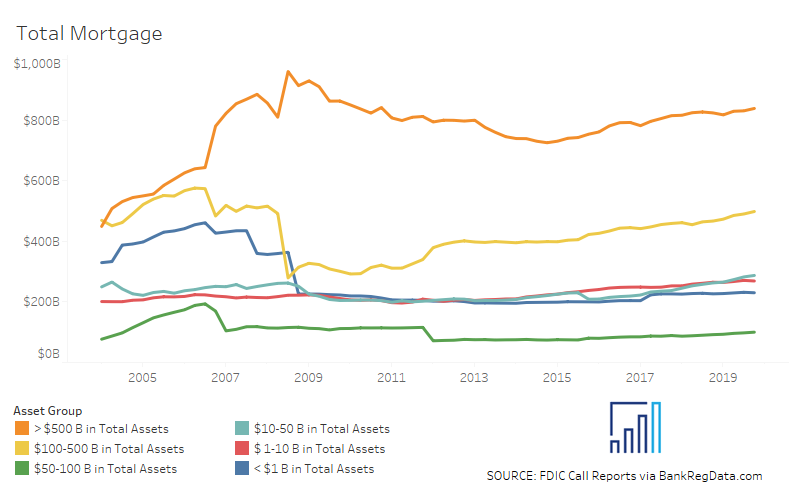

Figure 2

But what is causing consumer portfolios to shrink at the largest banks? It’s true that 2019 mortgage assets are 10% lower than pre-crisis levels, but mortgage assets have grown since 2014 and are similar to 2010 levels (Figure 2). There’s clearly more to this story. As it turns out, HELOC runoff is driving the broader consumer retreat at the Big 4. In 2019, Big 4 Banks had over $128 B in HELOC assets, a mere 35% of 2010 levels.

In fact, the retreat from HELOC is an industry-wide phenomenon (Figure 3). None of these banking segments increased HELOC concentration, nor have any even grown their HELOC portfolios (interestingly, smaller banks have grown consumer concentration despite this trend — more on this in a future post). Part of this trend is explained by changing consumer demand.

Figure 3

A prolonged low-rate environment likely encouraged borrowers to lock-in low interest rates with fixed-rate options rather than take a variable-rate HELOC. Additionally, banks have almost certainly tightened HELOC credit policy since the financial crisis. The pre-crisis strategy of combining simultaneous first and second lien loans in a purchase to lower down payment is all but extinct and loans from that era are running off. These factors combined with new FinTech players in this space (e.g. LendingTree offers home equity products)—which are not covered in Call Reports data—lead to a dramatic consumer assets runoff at the largest banks.

Where will home equity products go from here? If you think you know the answer, send me an email to discuss! AQN has worked with FinTechs offering innovative home equity products – if you would like us to take a look at your portfolio, give us a call. And of course, don’t forget to check back here next week for more BRD Insights.